Introduction:

It is paramount for all types of firms to invest into a costing system. Cost management enables a firm for continued progression to enable its budget to be more vigorous and ultimately more cost effective. This essay aims to outline the framework for the main two costing systems that determine the costs and predict the activities that are consuming the most resources. To retrieve these cost values, a firm can use one of the ‘traditional cost allocation’ method or the ‘activity-based costing’ method. Whilst scrutinising each method’s opportunities and challenges, its benefits and drawbacks will also be analysed.

Traditional Cost Allocation (opportunities and benefits):

The traditional cost allocation method has been described as the “absorption of production overheads (excluding selling and administration overheads) into product costs for stock valuation” (Letza and Gadd, 1994). The premise of this costing method is to calculate the indirect costs of a manufacturing business, with the notion of assisting managers make decisions beneficial for the organisation in terms of both costing and profitability. This is rendered by using only one overhead rate. Commonly, the machine hours or labour costs as these are directly relevant to the units produced, which can be shown by the following equation (Atrill and McLaney, 2015):

As there is only one overhead rate, there is an arbitrary allocation of excess costs to its total volume base. The CIMA Technical Services (2001) mentions the traditional costing system relies upon three stages to formulate its costs:

1. Accruing of all the costs within a department

2. Designate the indirect costs to the departments that are functional, from the total costs

3. The indirect costs calculated should then be applied to products and services.

Get Help With Your Essay

If you need assistance with writing your essay, our professional essay writing service is here to help!

These 3 stages allow for the costing system to align itself and be in accordance within the guidelines of the Generally Accepted Accounting Principles (GAAP) (Johnson, 2014). Moreover, for firms that produce only 1 product, this system allows for a quick and smooth implementation process. This is because the total volume allocation base will only cover the volume for the sole product in the firm’s entire production line (Hansen & Mowen, 2006).

Flaws of Traditional Cost Allocation & inception of ABC:

Over time the use of this traditional costing system has had its limitations and drawbacks. Whilst being in accordance with the guidelines of the GAAP, the traditional system for costing omits the costs created by customers. To use the results of costing in external financial reports, it excludes selling and administration overheads. The use of only one overhead rate eliminates many other potential costs associated within a firm’s entire production line, which can lead to unembellished imprecisions. (Atrill and McLaney, 2015)

In the past, the traditional approach in determining product costs has worked reasonably well. Overhead rates were typically of a much lower value for each direct labour than the rate paid to direct workers as wages or salaries. However, it is now becoming increasingly common for overhead rates to be between 5-10 times the hourly rate of pay due to the increased significance of overheads (Horngren et al, 1999). Even an insignificant change in the amount of direct labour worked on a job could massively affect the total cost deduced due to direct labour hours on the overhead cost loading. Moreover, overheads are still typically charged on a direct labour hour basis; overheads may not be closely related to direct labour however. (Atrill and McLaney, 2015)

Principles like these in the traditional system reduces the accuracy of the model, questioning the legitimacy of this costing approach. As a result, what arose was the opportunity for an alternative technique to overcome these flaws. This led to the inception of Activity-Based Costing (ABC)

Activity Based Costing:

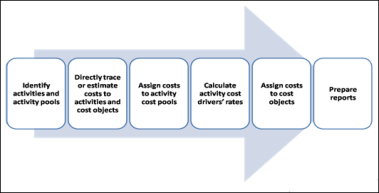

The inception of an ‘alternative costing system’ had been brought about in the early 1980s by Robert Kaplan – the first advocator of Activity-Based Costing. It was his aim to use more cost drivers to reduce the inaccuracies and inadequacies of traditional costing systems (Singer & Donoso, 2008). Activity-based costing is an accounting practice by which costs are allocated on the basis of a firm’s activities. The implementation of this costing system is explicated by a chronological, 5 stage template process, which Figure 1 shows.

The major amendments made to the traditional costing system are the multiple cost drivers and overhead rates that are identified. Identifying cost drivers holds as the imperative component towards a successful ABC system, for a more accurate and wholly reflective costs within a firm. The cause and effect relationship with activity costs acts as a basis for attaching these costs to a product or service (Atrill and McLaney, 2015). Created to forecast future costing, forward planning places managers in a more prominent position to assess the likely effect of new products and processes on activities and costs, leading to wider opportunities for firm managers (Horngren et al, 1999).

Activity-Based Costing – Opportunities and Benefits

Activity-based costing offers a wide plethora of diverging opportunities. Significantly, the system has been taken on and been made more relevant to service industries. In the absence of a direct material element, a service business’s total costs are more likely to be predominantly composed of overheads. A survey conducted investigating 176 UK businesses (from varying industries) with annual sales revenue greater than £50 million found overheads represent 51% of total cost for service providers. This is in stark contrast to 25% for manufacturers. These statistics certainly point towards the fact that ABC is an appealing proposition to adopt for firms that sell services rather than products (Atrill and McLaney, 2015).

ABC can be used as a powerful tool for continuous rethinking and dramatic costing improvement in not only the services and products, but also market strategies and processes (Jinga et al, 2010). When Chrysler was placed in a period of financial turbulence, it exalted its costing system to ABC in 1991 in attempts to catch up to its formidable competitors, Toyota and Ford Motor Company. Previously, the true costs of Chrysler were made to be 30 times larger than what had been calculated (Meador, n.d.). Post-ABC (after short-term struggle through inevitable transitional difficulty) Chrysler recovered to a competitive standpoint; the automotive firm claimed they have saved hundreds of millions of dollars to date. (The Economist, n.d.)

Similarly, the previously publicly-owned Royal Mail endorsed the ABC system to discover the cost of making postal deliveries, they identified 340 separate activities and subsequent cost drivers (Atrill and McLaney, 2015).

The implementation of ABC can present a strenuous challenge, but with astute and correct execution, a firm can reap fruitful benefits. Within 5 years of implementation of ABC, Dutch firm Wavin made this system part of its day-to-day management culture, playing a significant role in their ‘management excellence programme’. Wavin introduced ABC by linking it to a practical business application – ‘profitability management – which considered an ideal pilot area for learning about ABC, as well as establishing a deeper understanding for the relationship between product and customer profitability (Horngren et al, 1999).

However, by treating ABC as a short-term concept, Wavin ran into trouble. By operating on a day-to-day management culture, they concluded every effort should be made to calculate ABC for all products. The caveat was that their real emphasis should be placed in ensuring the decision-making processes would lead to the accuracy of ABC attributed to both customers and products. Consequently, with its products Wavin used a two-phased approach whereby customers were classified into separate cost drivers. This approach generated an overall cost/customer matrix which was utilised as a foundation for its managerial decisions, representing the most significant part of the company’s business (Horngren et al, 1999). Wavin’s implementation of ABC showed the relative unease for a firm to change its costing system, whereby the system has had many critics on its complex nature.

Criticisms/Shortcomings of ABC:

In spite of its main objective being to add accuracy and precision into costing schemes, from its inception ABC contained flaws. Analysing multiple overheads to identify cost drivers is time-consuming and costly. The cost of setting up the ABC system, as well as costs of running and updating it, must be incurred. The more overheads and cost drivers that are identified, the greater potential is associated with higher maintenance costs (Horngren et al, 1999). Should the firm’s operations be more complex and involve many activities and cost drivers, the longer the time spent to maintain this scheme. Thus, higher expenses should be paid towards its maintenance.

The implementation of this costing system also presents challenges. Managers need to be taught and prepared to facilitate these new schemes, which comes with external and additional training. Once more, the complexity of mastering the scheme can be taxing in terms of time consumption. Many firms have found it problematic to implement ABC to existing, traditional costing systems, where it is argued that it is more manageable for start-up firms to commence with ABC (Horngren et al, 1999). Furthermore, each firm looking to take on this scheme must have all its business components broken down into its discrete components to identify all potential cost drivers. Perfecting the art of this scheme requires prolonged training, which again is an expensive measure (The Economist, n.d.).

Comparing TCA to ABC:

Traditional cost allocation has been around since the 1870s, where its use as a system has been going for many more decades than its alternative ABC: its inception was in the early 1980s (Ben-Arieh & Qian, 2003). Interestingly a study claims that ABC is an additional costing system, not an alternative. When comparing different firms’ financial situations, it is highly likely that these firms do not have the exact same costing system. Some firms may use a traditional system with only one activity and cost driver associated to it, whilst others using ABC will have multiple activities and cost drivers: adding onto what the traditional system has (Narong, 2009).

Find Out How UKEssays.com Can Help You!

Our academic experts are ready and waiting to assist with any writing project you may have. From simple essay plans, through to full dissertations, you can guarantee we have a service perfectly matched to your needs.

View our academic writing services

ABC includes labour or product parts that can be identified whereas the traditional method arbitrarily accumulates salaries, expenses, and depreciations. (Blocher, 2006) For estimating costs, ABC is a more precise system as it nurtures managers in becoming more knowledgeable of the indirect resources which identifies and removes cost drivers that are of no marginal value. It also gives managers an insight into existing parameters that have generated demands. (Jones & Dugdale, 2002)

The traditional approach sees its overheads as rendering a service to cost units, the cost of which must be changed to those units. ABC on the other hand views overheads as being caused by activities, like operating a store to house the cost units. Since it is the cost units that cause these activities, it is thus the cost units that must be charged with the costs that they cause. A reason for the inception of ABC is within the way overheads are organised. The traditional approach has the overheads apportioned to product cost centres, whereas ABC has its overheads analysed into cost pools, with one cost pool for each cost-driving activity. (Atrill and McLaney, 2015)

The intention of ABC was neither to measure short-term variable costs nor provide a day-to-day guidance on process quality. With its ‘forward planning’ nature, using ABC to predict short-run costs overlooks the fact that costs are the results of spending decisions (Horngren et al, 1999). To its disadvantage, the traditional system, on the other hand, does not present non-financial information concerning the Small and Medium Enterprise (SMEs), perhaps displaying a slight negligence (Hilton, 2006).

Conclusions:

Whilst in theory there are two major approaches to choose from for a firm to undertake its costing decisions, there is no politically correct or preferred choice. Each costing system presents altering opportunities and challenges, where a firm ultimately has to choose dependent upon factors such as the firm’s industry. There has not been a major swell of manufacturing firms converting to implement ABC. Costing systems in the manufacturing sector are far more complexed, needing to convert materials into work in progress, than finished goods. However, large-scale manufacturing firms such as Siemens, Philips, Volvo and Ericsson made the brave decision in the 1990s to implement ABC. (Horngren et al, 1999) Yet 2 of these firms in Siemens and Philips have in today’s climate have lost a significant market share to they once had; whether this is attributed to ABC is another question.

It is important to note that the intended objectives of an ABC system at the time of implementation are likely to differ from its resulting consequences. The methodology behind ABC sets a company in a superior platform in terms of precision and accuracy, allowing managers to make more informed and knowledgeable for a firm’s long-term future.

References

Atrill, P. and McLaney, E. 2015. Accounting and finance for non-specialists. 1st ed. Harlow [etc.]: Pearson Education, pp.282-306.

Ben-Arieh, D. and Qian, L., 2003. Activity-based cost management for design and development stage, International Journal of Production Economics, 83,169-183

CIMA Technical Services. 2001. Activity-based management – an overview. [pdf]. CIMA Technical Briefing. Available from: www.cimaglobal.com/technicalreports [Accessed 23 March 2017]

Hansen, D. and Mowen, M. 2006. Cost management: accounting and control. Mason, OH: London: Thomson/South-Western.

Hilton, R.W. 2006. Cost Management: Strategies for Business Decisions, 3rd Ed. McGraw Hill, New York

Jinga, G., Dumitru, M., Dumitrana, M. and Vulpoi, M. 2010. Accounting systems for cost management used in the Romanian economic entities, Accounting and Management Information Systems, 9(2), pp.242-267.

Johnson, R., 2014. Traditional Costing Vs. Activity-Based Costing | Chron.com. Available at: http://smallbusiness.chron.com/traditional-costing-vs-activitybased-costing-33724.html [Accessed March 24, 2017].

Jones, T. C. and D. Dugdale. 2002. The ABC bandwagon and the juggernaut of modernity. Accounting, Organizations and Society 27(1-2): 121-163.

Letza, S. and Gadd, K. 1994. Should Activity†based Costing be Considered as the Costing Method of Choice for Total Quality Organizations?. The TQM Magazine, 6(5), pp.57-63.

Martin, J. (n.d.). ABC vs TOC. [online] Maaw.info. Available at: http://maaw.info/ArticleSummaries/ArtSumHolmen95.htm [Accessed 28 March 2017].

Meador, D. (n.d.). ABC: Initiating Large-Scale Change at Chrysler – The Systems Thinker. [online] The Systems Thinker. Available at: https://thesystemsthinker.com/abc-initiating-large-scale-change-at-chrysler/ [Accessed 28 Mar. 2017].

Narong, D.K. 2009, ‘Activity-Based Costing and Management Solutions to Traditional Shortcomings of Cost Accounting’, Cost Engineering, 51, 8, pp. 11-22, Business Source Premier, EBSCOhost, [Accessed 26 March 2017]

Singer, M. and Donoso, P. 2008. Empirical validation of an activity-based optimization system, International Journal of Production Economics, 113, pp.335-345

The Economist. N.d. Activity-based costing. [online] Available at: http://www.economist.com/node/13933812 [Accessed 26 Mar. 2017].

ABC – WordPress. (n.d.). Activity-Based Costing (ABC). [online] Available at: https://allearth.wordpress.com/education/cost/abc/ [Accessed 30 Mar. 2017].

Cite This Work

To export a reference to this article please select a referencing style below: